Building a New Home vs Buying an Existing Home: What You Need to Know

Purchasing commercial property within your SMSF allows business owners to grow retirement savings while potentially leasing the premises back to their own business. This strategy offers rental income, concessional tax treatment and long term capital growth, but must comply with strict superannuation rules. Property must be acquired at market value, structured correctly and, if borrowing, set up under a Limited Recourse Borrowing Arrangement. Residential Lending Group connects you with trusted SMSF specialists to ensure your structure and compliance are handled correctly.

Purchasing Commercial Property Within an SMSF: What Business Owners Need to Know

Choosing between building a new home and buying an existing property depends on your priorities, timeline and budget. Building offers custom design, modern features and lower early maintenance, but involves longer timeframes and potential delays. Buying an existing home provides faster move in, established neighbourhoods and clearer market value, though renovation or repair costs may apply. Understanding the process, costs and risks of each option helps you decide which path suits your lifestyle and financial goals.

Limited Recourse Borrowing in SMSFs: What You Need to Know

Thinking about setting up a Self-Managed Super Fund? An SMSF gives you direct control over your retirement investments, including property, but comes with strict responsibilities and compliance requirements. This guide outlines the key steps involved and explains how Residential Lending Group can connect you with trusted SMSF specialists to support your setup and financing journey.

Understanding the Difference Between SMSF Loans and Regular Home Loans

SMSF loans and regular home loans both finance property, but they operate under different rules. An SMSF loan is taken out by your super fund for investment property and must meet strict superannuation regulations. A regular home loan is taken out by individuals for owner occupied or investment use. Residential Lending Group connects you with trusted SMSF specialists to help you choose the right structure for your goals.

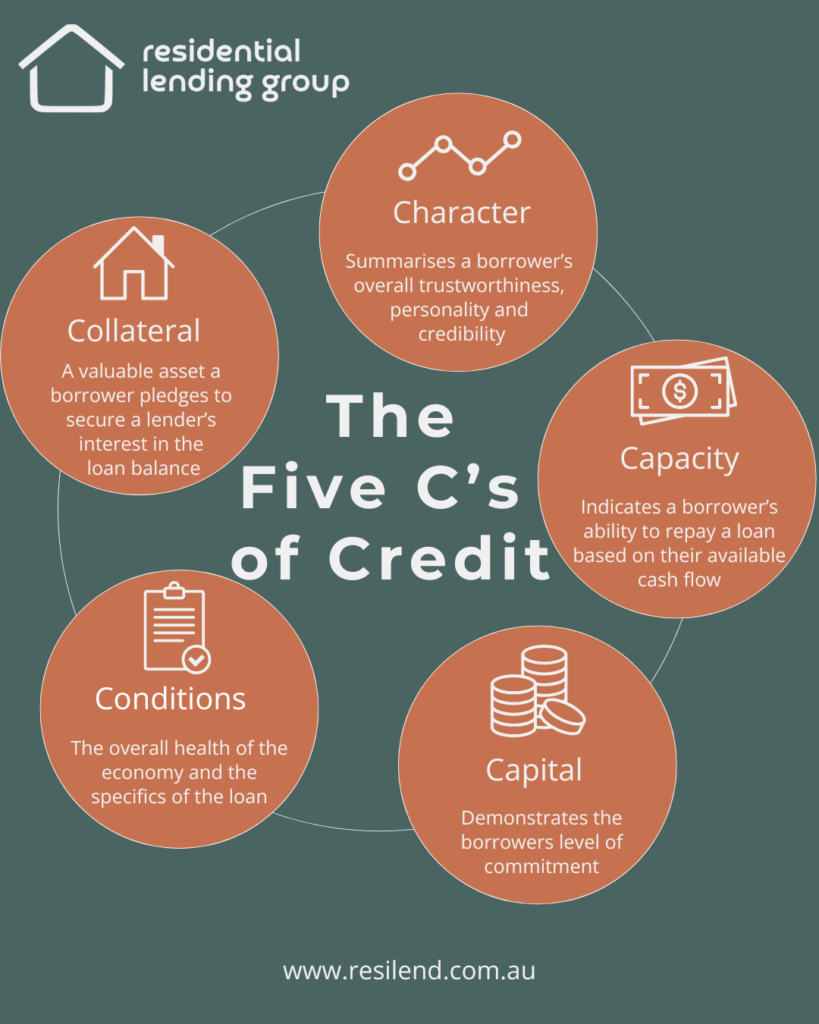

The 5 C’s of Credit

This graphic explains the five key factors lenders assess when reviewing a loan application. Character reflects your credit history and reliability. Capacity measures your income and ability to repay the loan. Capital refers to your savings and financial contribution. Collateral is the asset used to secure the loan. Conditions consider the broader economic environment and the purpose of the loan. Together, these five elements determine overall credit strength.