Library

Investing in Property: What You Need to Know

Investing in Property: What You Need to Know

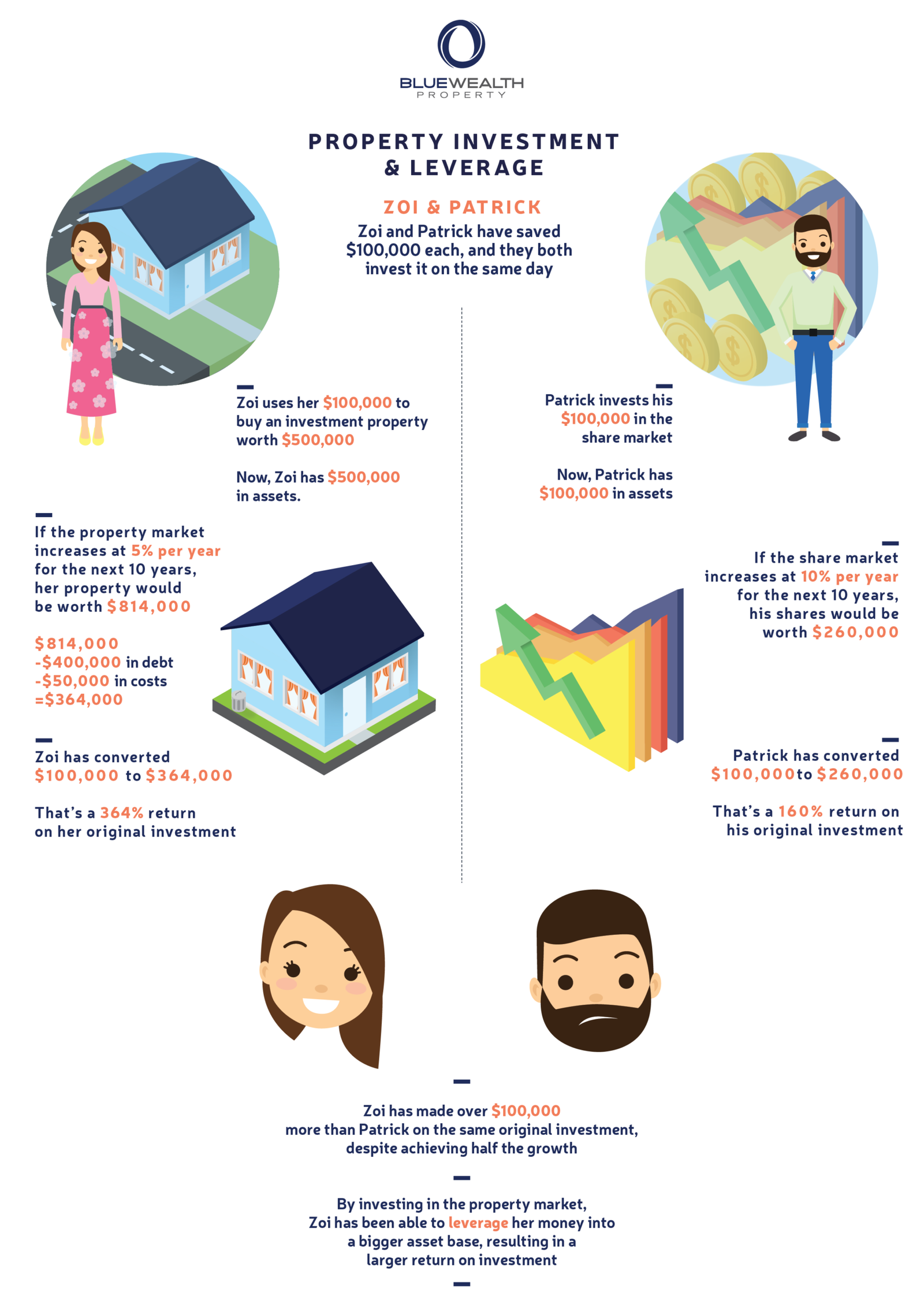

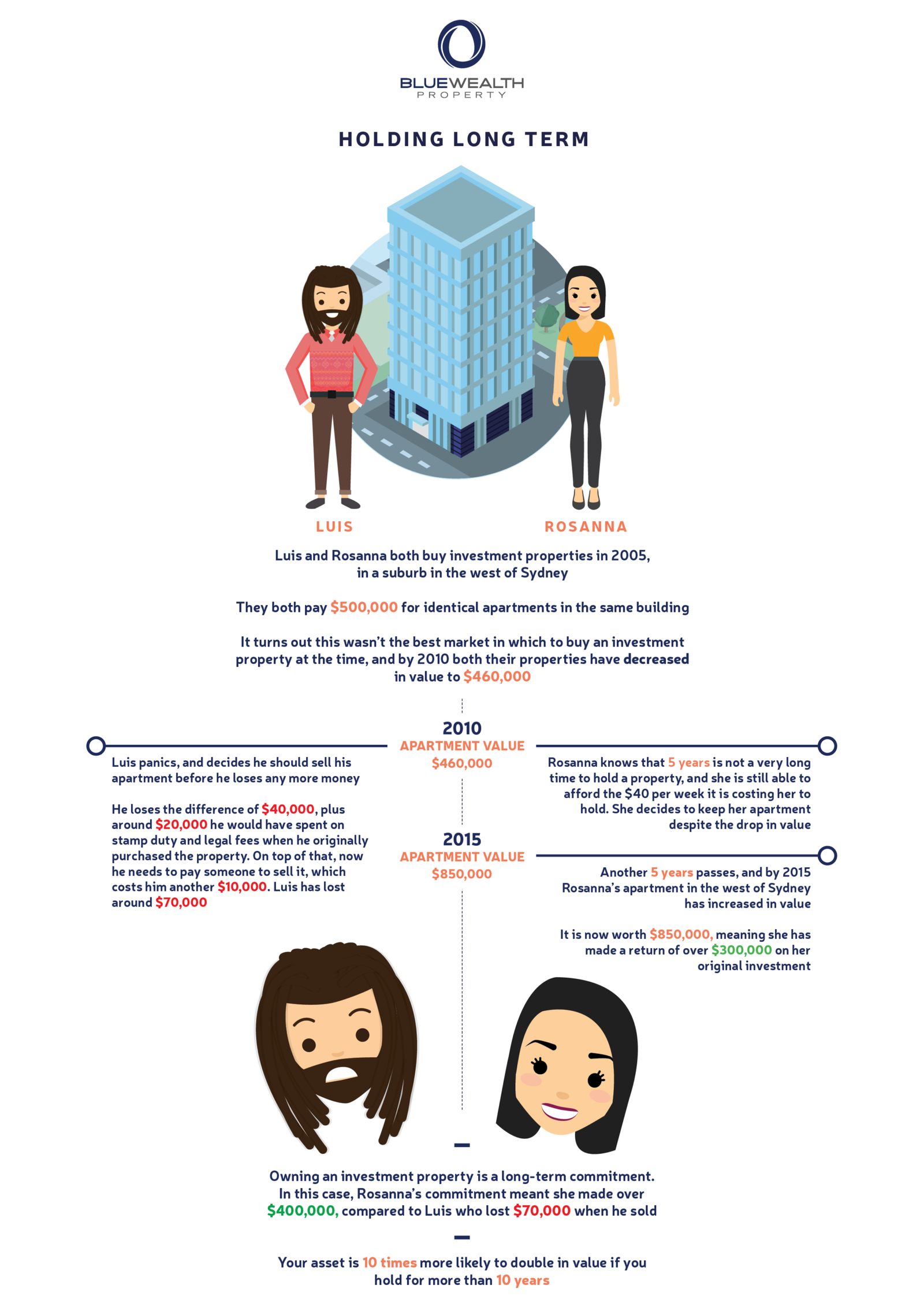

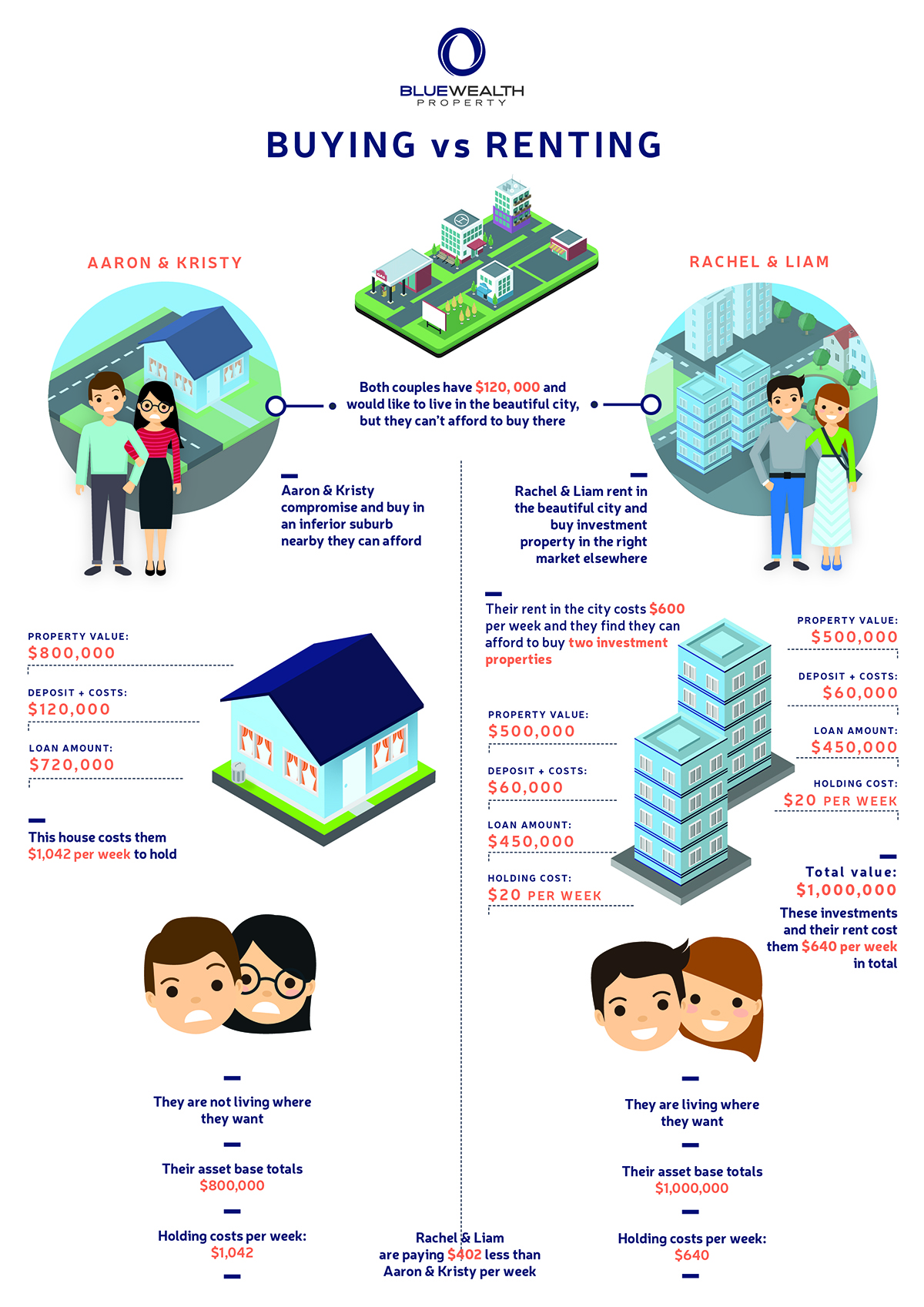

Property investment offers potential growth and income, but it requires careful planning. Explore risks, tax considerations, loan structures, and the value of building the right advisory team.

Stamp Duty and Its Impact on Lending

Stamp duty is a major upfront cost that affects your deposit, LVR, and borrowing capacity. Learn how concessions work and why planning for this expense is critical.

Saving a Deposit: Understanding Genuine Savings

Lenders assess your savings history to confirm financial discipline. Understand what counts as genuine savings, what does not, and how this affects high LVR loan applications.

Understanding Refinancing: What It Means and How It Can Benefit You

Refinancing replaces your current home loan with a new one to better suit your goals. Learn how lower rates, equity access, and new loan features may improve your financial position.

Using Equity as a Deposit for a Property: What You Need to Know

Using equity in your existing property can help fund the deposit for your next purchase. Learn how lenders assess equity, LVR limits, risks, and borrowing capacity before leveraging your home to buy again.

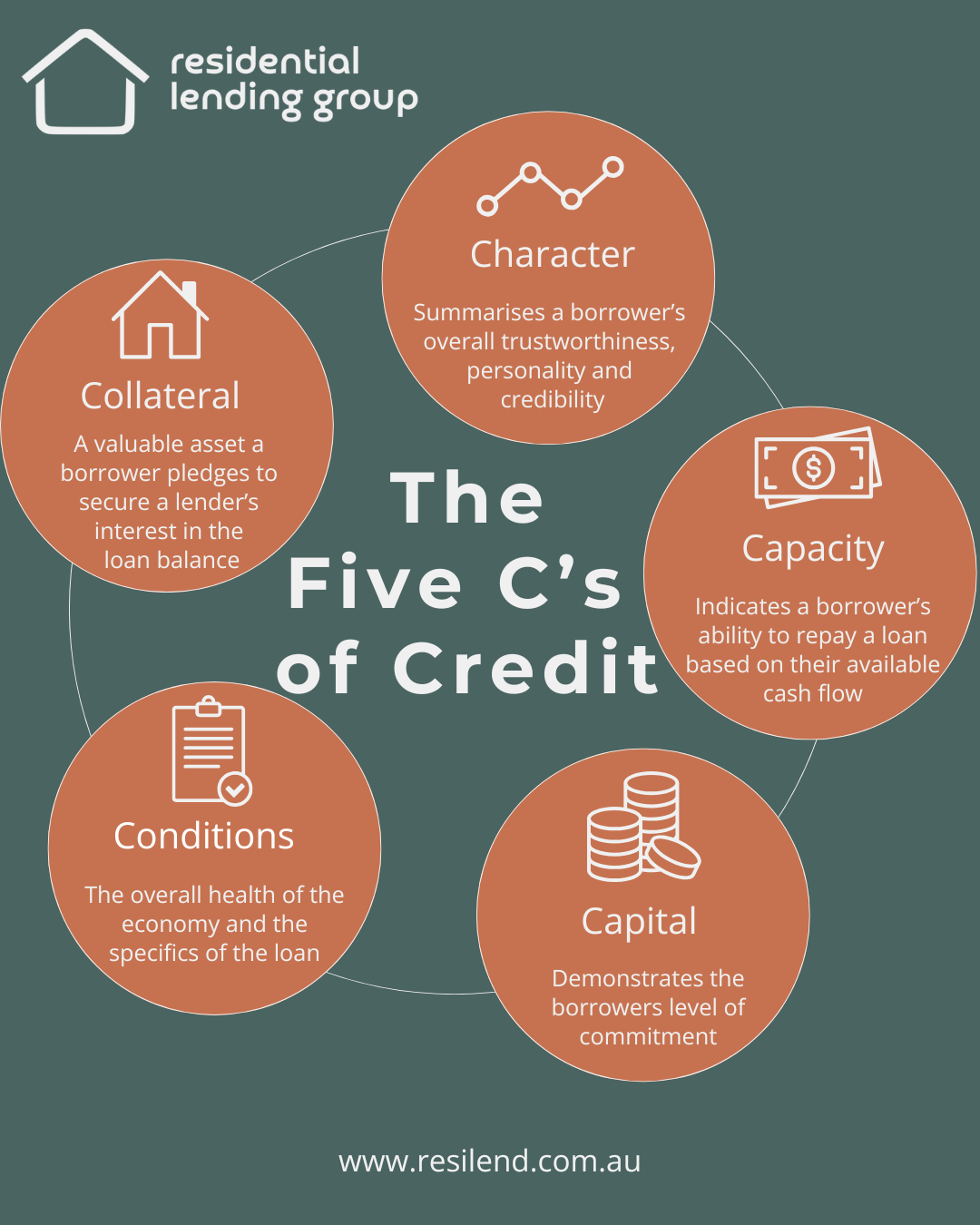

Understanding Credit Ratings and Defaults: How They Impact Your Lending Options

Understanding the Difference Between an Offset Account and a Redraw Facility

Both features help reduce interest, but they function differently. Understand how offset accounts and redraw facilities compare so you can manage your loan effectively.

Different Types of Home Loans: Basic Variable, Standard Variable, and Fixed Rate Loans

Different loan types offer varying levels of flexibility and repayment certainty. Explore how variable and fixed options compare before choosing your structure.

Understanding Alt Doc Loans and Loans for the Self-Employed

Alt Doc loans provide flexible income verification options for self-employed borrowers. Explore how alternative documentation works and when this option may suit your circumstances.

Bridging Loans: How They Can Help Navigate Settlement Challenges

Buying before selling can create settlement timing pressure. Learn how bridging finance works, who it suits, and what to consider before committing.

Understanding Offset Accounts: How They Can Help You Save on Your Home Loan

Principal & Interest vs Interest Only Repayments: What You Need to Know

Understanding Investment Loans and Owner Occupied Loans

The purpose of your property affects interest rates, repayments, and tax considerations. Understand the key differences between investment and owner occupied loans.

Lenders Mortgage Insurance (LMI) Waivers: What You Need to Know

Some borrowers may qualify for an LMI waiver based on profession or financial profile. Discover who may be eligible and how this can reduce upfront costs.

Understanding Lenders Mortgage Insurance (LMI): What You Need to Know

LMI protects the lender when you borrow with less than a 20 percent deposit. Learn how it works, what it costs, and how it affects your total loan amount.

GST Registration and Finance Lending: What Self-Employed Clients Need to Know

Self-employed borrowers may need GST registration to meet lender requirements. Understand turnover thresholds and how GST status can influence your loan application.

The First Home Super Saver Scheme: A Guide for First Home Buyers

The FHSSS allows eligible buyers to use voluntary super contributions toward a deposit. Discover how the scheme works, contribution limits, and key considerations before applying.

Australian Government 5% Deposit Scheme Explained

Buy your first home with as little as a 5 percent deposit and avoid LMI. Learn how the government guarantee works, who qualifies, and what property limits apply.